PZ Cussons: Valuing a Nigerian Consumer Product Company

Background & Company History

CZ Cussons is a British company with African roots. George Paterson and George Zochonis set up a trading post in Sierra Leone, trading goods between West Africa and the UK in 1884. The company is still publicly traded in the UK and has global revenues now, but has created subsidiaries in Nigeria and Ghana that it controls but are independent companies. PZ Cussons Nigeria has well known brand names and an established distribution base and you can get some information about it at its website.

Operating History

PZ Cussons Nigeria is a stand alone company but it is controlled by the British parent (PZ Cussons UK) which owns about 73% of the company. While the company has a long history in Nigeria and well established brands, its operating history in this century has been checkered:

In fact, the years since 2008 have been awful, with nominal revenue growth (in Naira) only 1.55% (which given the inflation rate of 10% plus, indicates that the company is shrinking) and is margins have been lower.

While the company (and analysts following it) have been quick to blame the problems on currency devaluation, political risk and lower oil prices (reducing disposable income in the hands of Nigerians), the problems run deeper. The company has a broken operating model, dependent on inputs from outside Nigeria while almost all of its revenues are in Nigeria. The company is trying to move its inputs to local sources but that will take time and be expensive and it really has no scope for growing outside Nigeria because the parent company has subs in other sub-Saharan African countries and will not allow PZ Nigeria to compete in them.

Spinning a Story and putting into Numbers

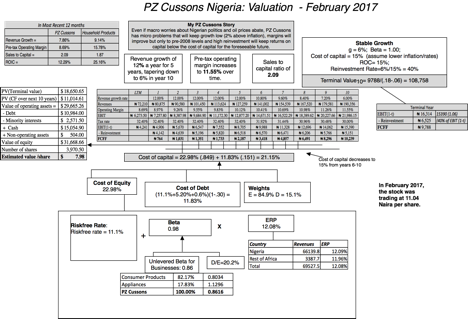

Even if macro worries about Nigerian politics and oil prices abate, PZ Cussons has micro problems that will keep growth low (2% above inflation), margins will improve but only to pre-2008 levels and high reinvestment will keep returns on capital below the cost of capital for the foreseeable future.

Putting these valuation inputs into a DCF, the value per share that I get is 7.98 Naira/share, well below the 11.04 Naira per share that the stock is trading at. You can download the spreadsheet that contains the valuation here.

http://www.stern.nyu.edu/~adamodar/pc/country/PZCussons.xls

Pay heed to the fact that the estimates are all in Nigerian Naira, explaining both the high growth rates (both for the foreseeable future and forever) and the high cost of capital.

The Valuation as a Picture

It is often difficult to see how your inputs become value in a conventional spreadsheet. So, I have converted my excel spreadsheet into a picture below. You can see how my valuation inputs now become cash flows, discount rates and eventually a value.

I will end with a confession. I know very little about the company, its management and about the Nigerian market. That can be a plus, since I entered the valuation with no bias, but it can be a minus, since I could be missing something very significant with the company.